in Aircraft values, Lease Rates & Returns , Lessors & Asset managers , Airline trends & analysis

Thursday 11 June 2026

H1: Ishka webinar takeaways: the muted reaction to the jet fuel crisis

The key takeaways from this week’s Ishka Airfinance H1 webinar: Midlife narrowbody lease rates decline from their peaks, airlines reduce growth plans.

As the halfway point of the year approaches and the war in Iran enters its 14th week, the ramifications of the conflict and the ensuing oil shock are impacting midlife narrowbody lease rates for lessors, while also forcing airlines to take action to offset high fuel costs.

Ishka summarises several of the key takeaways from its webinar held this week.

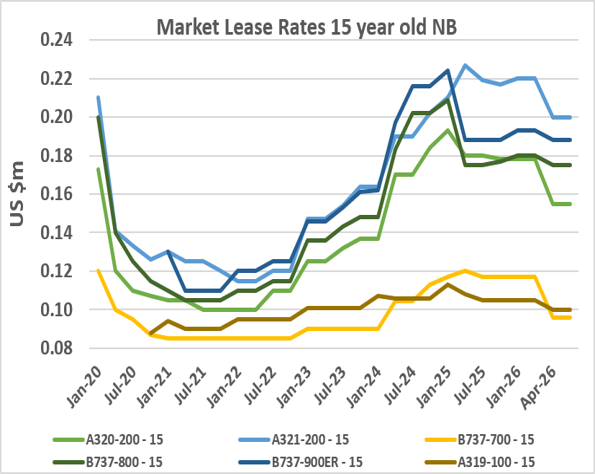

Midlife narrowbody lease rates weaken while values stabilise

Lease rates and values for new build narrowbodies and widebodies remain stable, but midlife previous-tech narrowbody lease rates are continuing to soften, according to Ishka’s aircraft appraisal arm.

Previous-tech narrowbody lease rates recovered strongly post-pandemic due to demand for aircraft to cover for OEM delays, supply chain constraints, and significant engine issues on younger aircraft, and peaked last year, according to Ishka research. Demand for midlife narrowbody aircraft is still strong, but a combination of factors, including the Iran war and high fuel prices, have paused some fleet plans which has started to bring rates down further (see Insight).

Eddy Pienaziek, Head of Advisory, highlights that the pull back is also partially caused by the influx of available aircraft following the liquidation of Spirit Airlines, creating a softening in demand. Eyes are firmly on the Spirit fleet to see how quickly the serviceable aircraft will be digested by the market, which will serve as a bellwether for the near term future of the midlife narrowbody market.

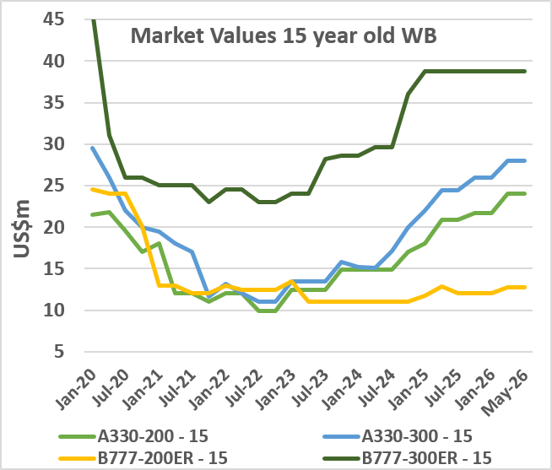

Meanwhile, with respect to 15-year-old widebody market values, there may be more growth to come following a steady increase over the last three years, with the exception of the 777-200ER, where high maintenance costs and competition with newer aircraft types have limited its value growth. In terms of 15-year-old widebody lease rates, numbers have improved as more aircraft have returned to service, with, for example, very few A330-300s currently parked.

As for market values, midlife narrowbody values are still stable, helped by the ongoing appreciation of narrowbody engine values, but this could change. Some engine traders anticipate that previous-tech engine values and lease rates will also be affected by the continuation of the Iran war, aas the effects of the conflict could force weaker airlines to readjust their fleet plans or even restructure (see Insight). Others disagree, arguing that previous-tech narrowbody engine lease rates are staying stable for the main.

Fuel shock forces airlines to raise fares and cut capacity

Airlines have revised growth expectations as a result of the high fuel prices stemming from the Middle East conflict (see table below). As high fuel prices continue, some airlines have taken measures including restructuring schedules, cancelling routes, and increasing fares or baggage prices, among other measures.

The rise in jet fuel prices is coinciding with an already elevated cost environment for airlines. While this varies by region, generally non-fuel expenses have been relatively high in recent years driven by supply chain issues affecting maintenance and aircraft ownership costs but also by higher labour expenses and airport charges, among other factors.

Siddharth Narkhede, Head of Airline Analysis, notes that fares have gone up across the board in response to the cost pressures. Nonetheless, it is unlikely that the increase will fully cover the cost burden so margins and cash flows will be affected. There also remains a risk of demand destruction if fares stay too high or rise further, especially in emerging markets.

“Generally, airlines have said demand has held up despite the higher fuel prices, and the strength of the premium and corporate in some markets has helped to shield or cover up the cost increases,” says Narkhede. “There's been, however, some softening signals as well, particularly changes in booking behaviour that a lot of the European airlines have reported, so shorter booking windows, some softness in some markets, or some resistance to hardy airfares.”

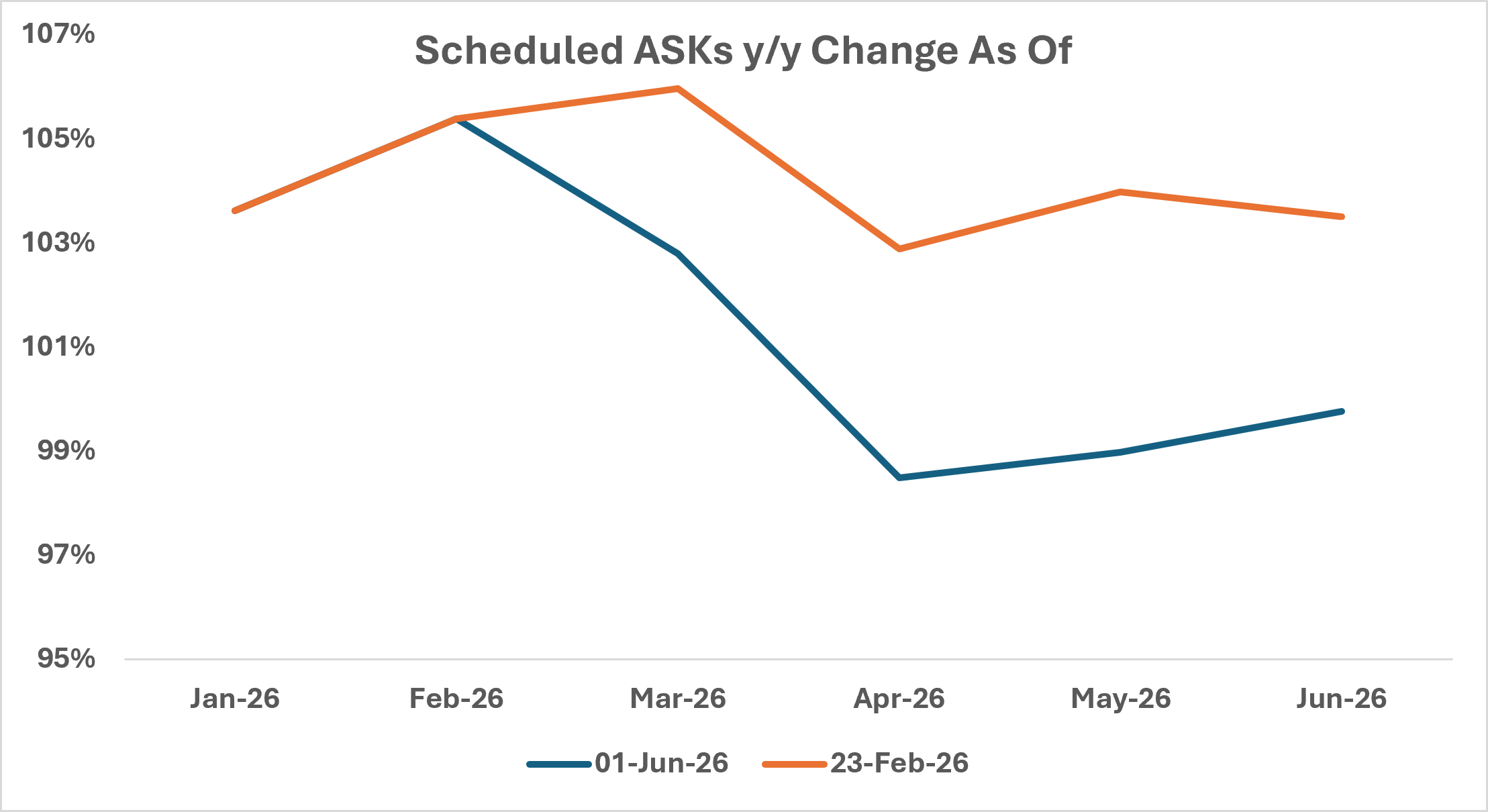

As the ASKs chart below shows, some airlines have reduced capacity for the near term, with a decline from Q2 2025, and while fluctuations in scheduled capacity are not a rare phenomenon, the adjustments made by airlines are symptomatic of the pressure that they are facing during this crisis. The lack of growth within the scheduled ASKs is a key indicator that airlines are facing difficulties. (Note: this chart includes the Middle East’s capacity reductions, which has a strong impact on the results).

The Ishka View

Outside of the Middle East, the Iran war has had arguably a less severe impact on airlines operations than some initially feared. Airlines have revised growth expectations, but it is the continuing uncertainty of the war (and its impact on fuel-price) which is the big difficulty for airline fleet managers. Even if the war ended tomorrow, the fuel market would remain volatile until the next year at least.

As a result, attention will be locked onto airline results in late Q3 and into Q4 to truly understand how the crisis has fully impacted airlines this year and the likelihood, or not, of any near-term airline restructurings. As has been stressed before by Ishka Airfinance’s Airline Credit Team, Middle Eastern airlines are at the centre of the conflict, but many have strong balance sheets, and implicit state support to help weather the current conflict. But, the airlines across the world who entered the crisis with pre-existing weaknesses in their operations and balance sheets remain more vulnerable.

Sign in to post a comment. If you don't have an account register here.