Against a backdrop of higher jet fuel prices and growing SAF blending mandates, European airlines are facing another significant cost increase in 2026: compliance with emissions trading systems (ETS). Although allowance prices in these market-based carbon schemes – in which operators must surrender emissions permits corresponding to their carbon output – are influenced by a wide range of factors, one reality is unavoidable. From 2026 onwards, airlines covered by the EU ETS and UK ETS will receive no free allowances to offset their emissions.

This report reviews the evolution of the EU ETS and UK ETS costs for airlines since their inception and quantifies the potential cost impact for operators in 2026.

The sun sets on free allowances

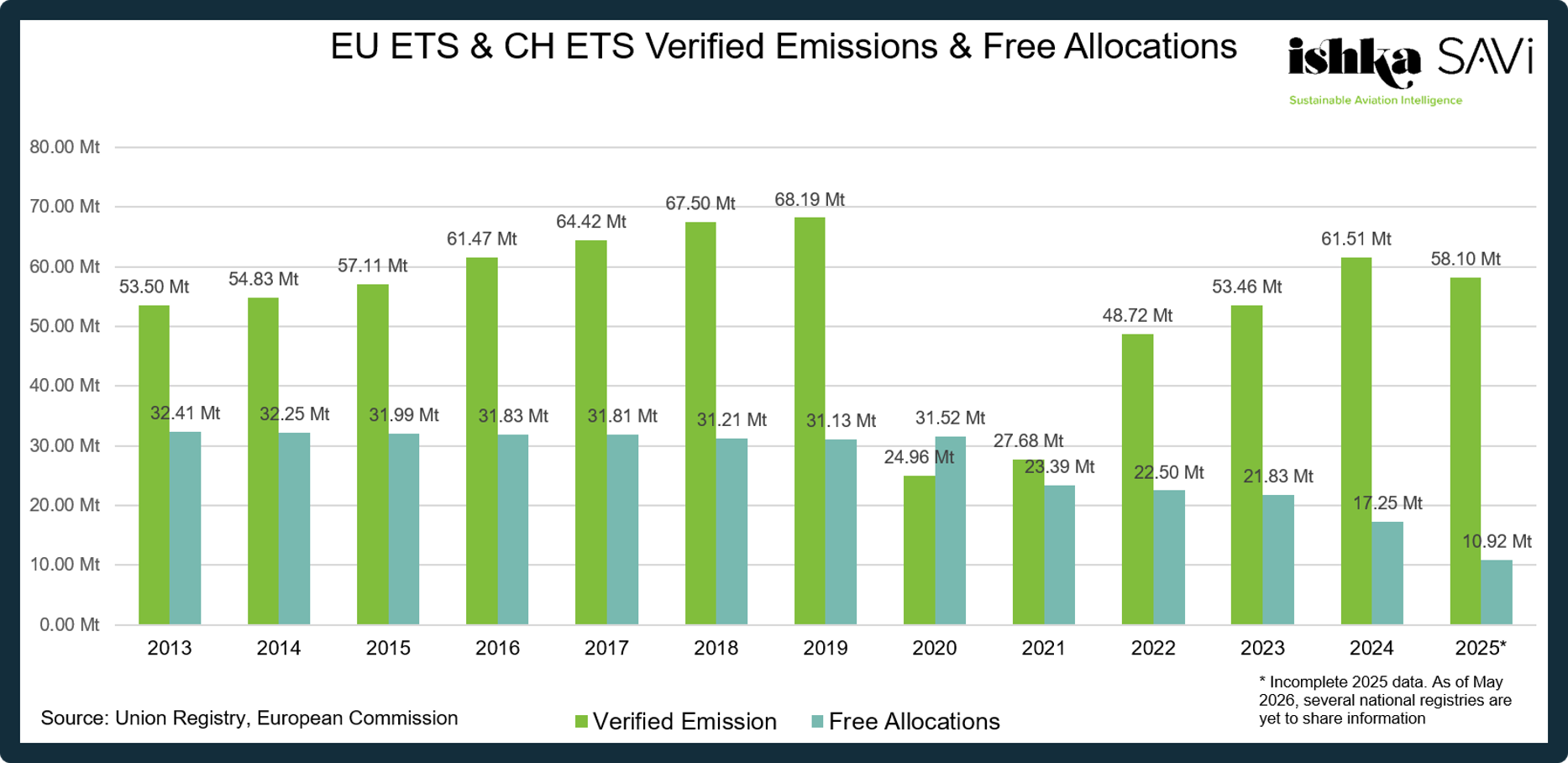

Note: 2025 verified emissions remain incomplete, with emissions reported to the French ETS authority yet to be included. This leaves out airlines such as Air France, Transavia France, Air Corsica, Corsair, or FedEx (whose European operations report emissions through France). UK emissions are included in this chart until 2020 (inclusive), as the UK participated in the EU ETS aviation sector during that period, including the 2020 Brexit transition year. From 2021 onwards, UK aviation emissions are no longer part of EU ETS totals and are instead covered under the UK ETS, creating a structural break in the time series (see chart below for UK ETS). This chart covers both EU ETS and CH ETS (the Swiss ETS) verified emissions and free allocations, as both systems are linked.

Note: 2025 verified emissions remain incomplete, with emissions reported to the French ETS authority yet to be included. This leaves out airlines such as Air France, Transavia France, Air Corsica, Corsair, or FedEx (whose European operations report emissions through France). UK emissions are included in this chart until 2020 (inclusive), as the UK participated in the EU ETS aviation sector during that period, including the 2020 Brexit transition year. From 2021 onwards, UK aviation emissions are no longer part of EU ETS totals and are instead covered under the UK ETS, creating a structural break in the time series (see chart below for UK ETS). This chart covers both EU ETS and CH ETS (the Swiss ETS) verified emissions and free allocations, as both systems are linked.

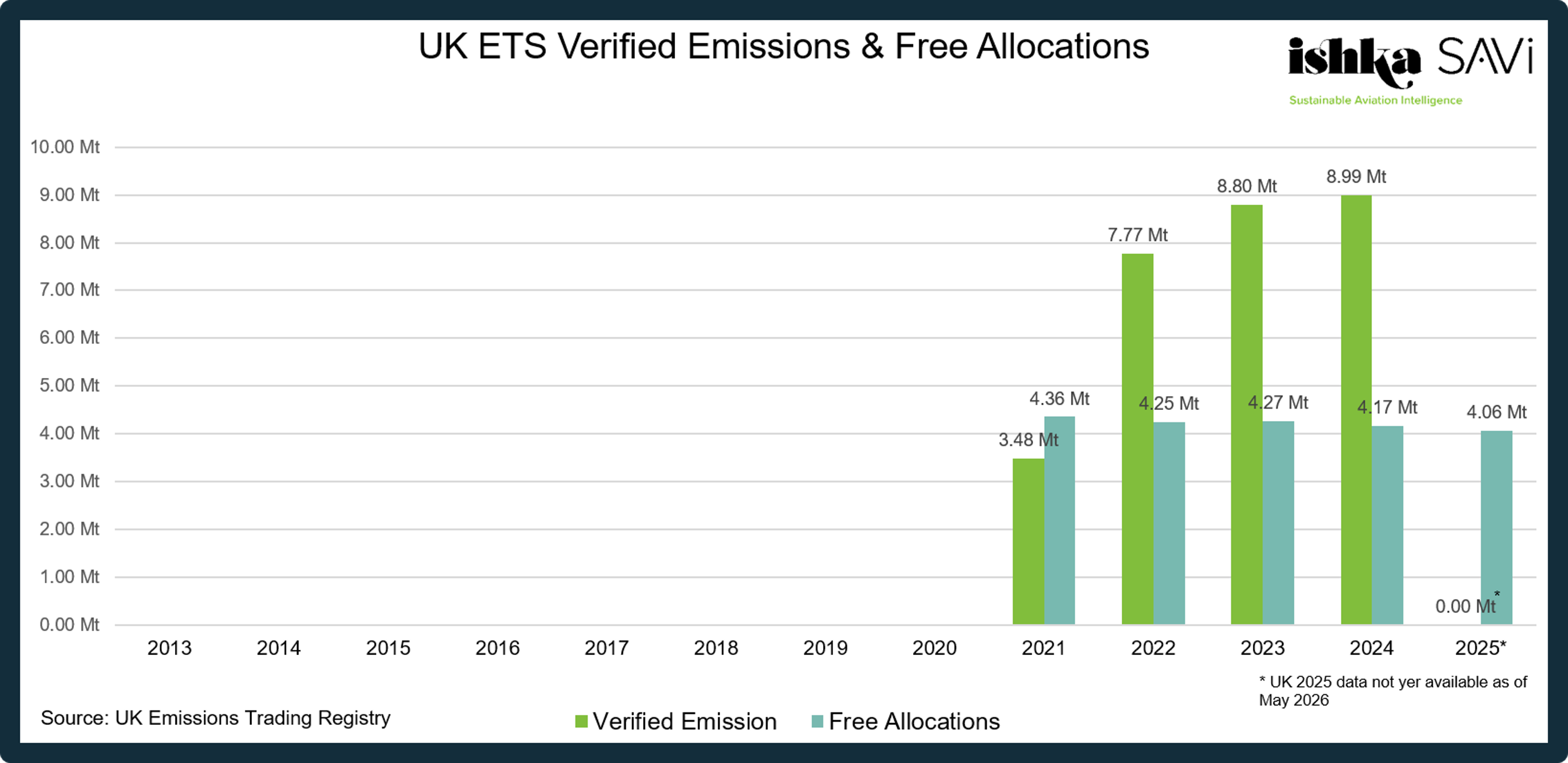

Note: For UK emissions prior to 2021, see EU ETS chart above (pre-Brexit transition). The UK has yet to publish a 2025 verified emissions number.

Note: For UK emissions prior to 2021, see EU ETS chart above (pre-Brexit transition). The UK has yet to publish a 2025 verified emissions number.

The allocation of free emissions allowances for airlines will be phased out in the EU, UK, and CH ETS by 2026, significantly increasing the compliance exposure for European airlines, particularly those with heavy intra-European operations. In the EU and CH ETS, which are already linked, this phase-out is gradual, and started with a reduction to 25% free allowance allocation in 2024, 50% in 2025, and 100% this year. For the UK, the end of the free allowance allocation is more abrupt, from a relatively stable annual free allocation since 2021 to zero this year.

The goal of the phase-outs is to strengthen the carbon price signal facing airlines, thereby increasing the incentive to reduce emissions and invest in cleaner technologies. Airlines operating more fuel-efficient fleets will pay comparatively less for their emissions than rivals flying the same routes*.

The concept of ‘free’ ETS allowances for airlines will continue to exist, however, in the shape of 20 million SAF allowances – allocated to operators based on a first-come, first-served basis to cover in part or full the price difference between uplifted SAF and conventional jet fuel. A summary of 2024 allocations of SAF free allowances ($117 million in that year) is available here. This allocation of free SAF allowances could grow. As part of measures against the recent increase in fossil energy prices, the European Commission will consider extending aviation’s ETS SAF support by “volume and duration”.

* Only between city pairs, not connecting traffic. One-stop and multi-stop journeys to destinations outside of the UK and EEA countries, (e.g. Toulouse to Tokyo, a city pair with no direct flights) may be exposed to competition distortion, as passengers connecting via European hubs (e.g. Paris or Frankfurt) rather than non-European hubs (e.g. Istanbul) will pay more in ETS-related costs regardless.

Higher and more volatile ETS prices

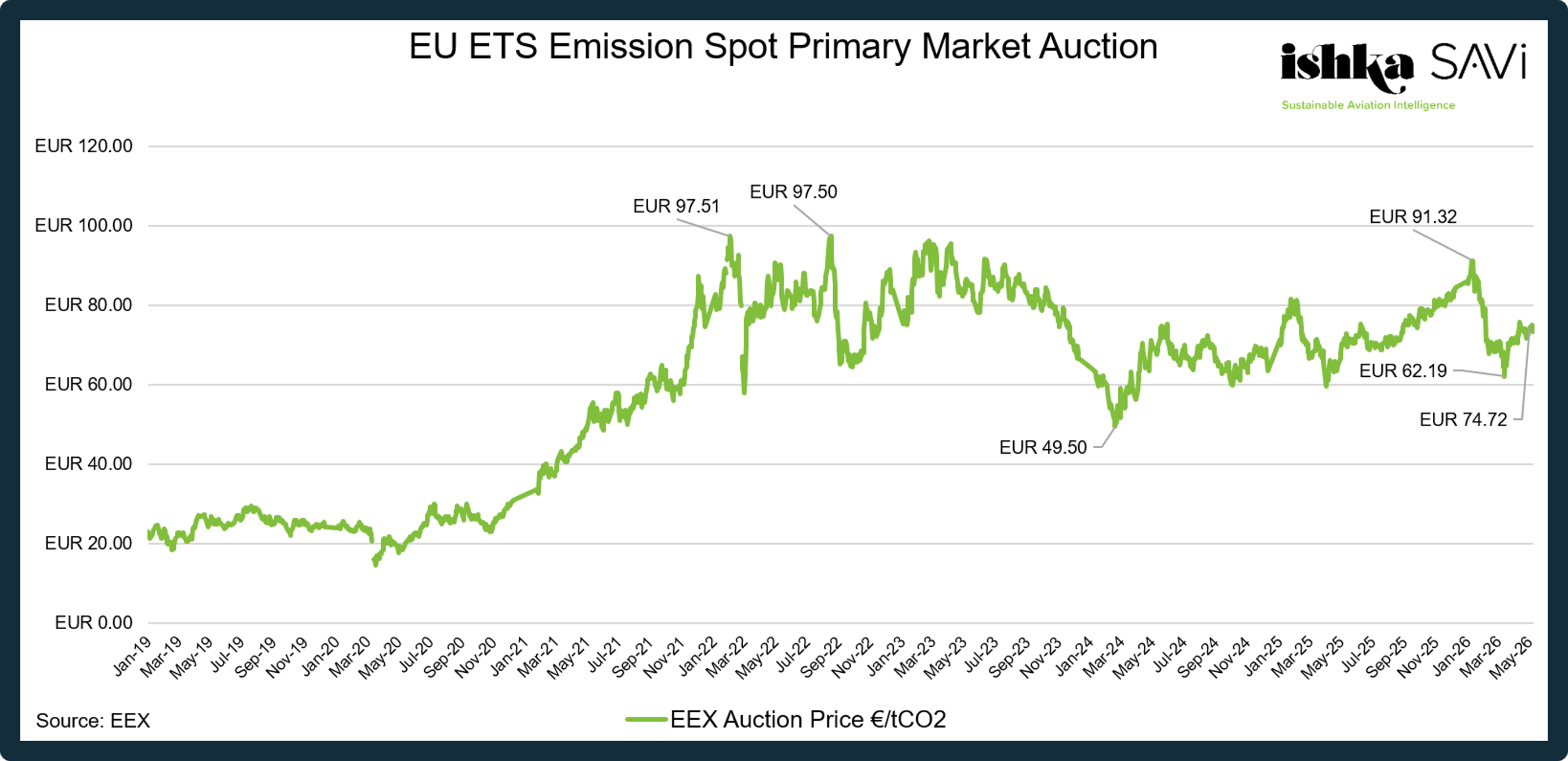

Note: Both of these charts show primary auction prices for EU ETS allowances (EUAs) and UK ETS allowances (UKAs), respectively managed by EEX and ICE. Spot trading of allowances between market participants occurs at different prices, although these typically track auction clearing prices closely and move in line with broader market fundamentals.

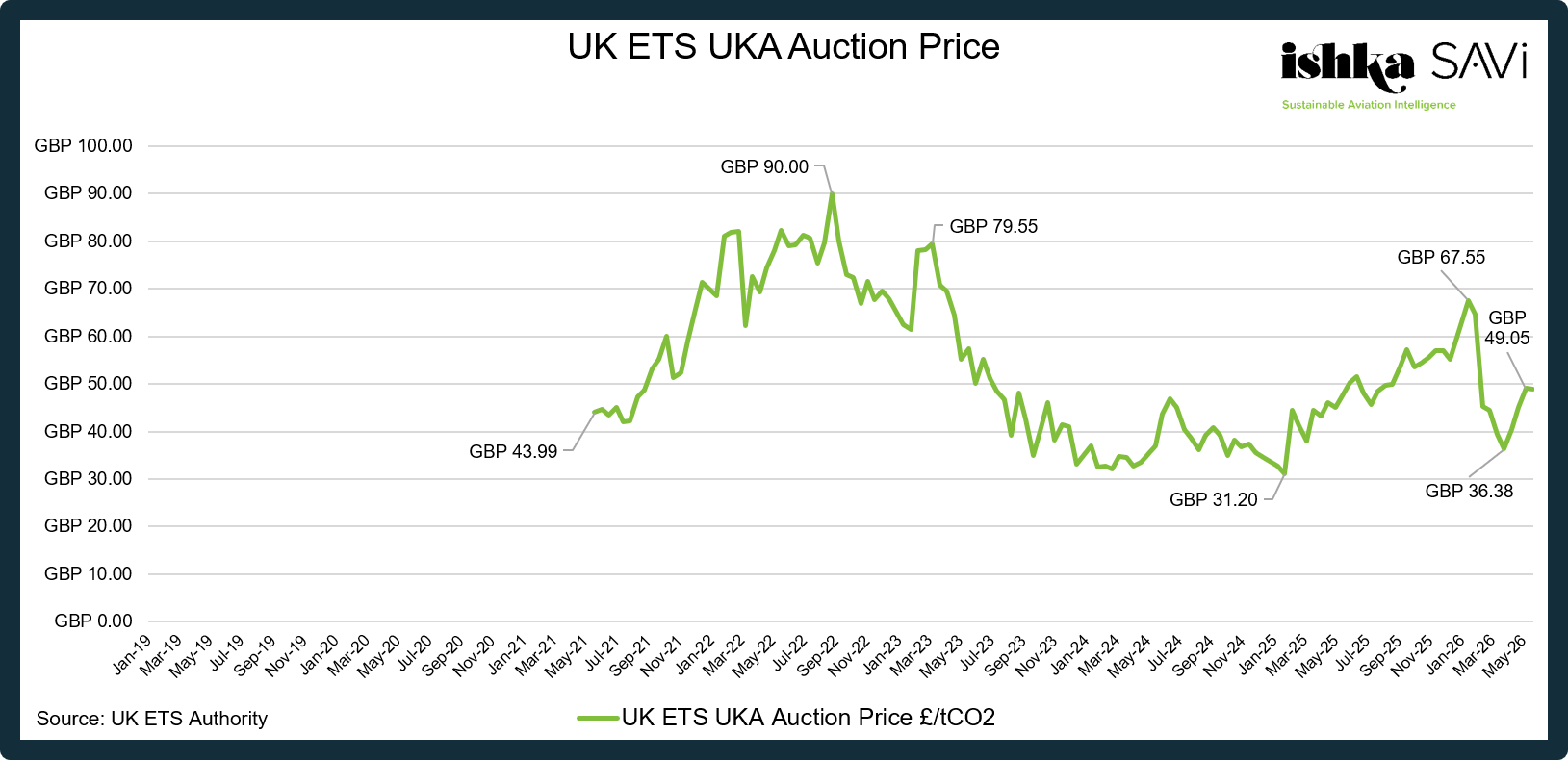

Note: Both of these charts show primary auction prices for EU ETS allowances (EUAs) and UK ETS allowances (UKAs), respectively managed by EEX and ICE. Spot trading of allowances between market participants occurs at different prices, although these typically track auction clearing prices closely and move in line with broader market fundamentals.

The progressive rise in ETS costs for airlines has been largely driven by the phase-out of free allowances, as this Q3 2025 Ishka SAVi analysis of airline financials confirms. However, the market price of emissions allowances has also risen considerably since 2021, driven by tighter emissions caps, policy reforms under the EU's Fit for 55 package, rising expectations of future carbon scarcity, and increased participation from financial investors.

The calendar-average price of primary auction EU ETS allowances has risen from around €24 per tonne ($28/t) in 2019 and 2020, to €54/t ($63/t) in 2021, €80/t ($93/t) in 2022, €83/t ($97/t) in 2023, €64/t ($74/t) in 2024, and €73/t ($85/t) in 2025. In the UK ETS, allowances have been priced cheaper than in the EU, averaging £52/t ($70/t) in 2021 (its first year), £75/t ($101/t) in 2022, £53 ($74/t) in 2023, and £37.18 ($50/t) in 2024, and £73 in 2025 ($98/t).

For the EU ETS, the picture since 2020 is largely one of high volatility, owing to changing economic conditions, energy market disruptions (Covid-19, Russia’s invasion of Ukraine) and policy reforms (such as the EU Fit for 55 package). Prices rose sharply in the post-pandemic economic recovery, as high gas prices forced a switch to higher coal shares with more emissions in the energy sector. There was also a tightening of emissions caps across sectors, a design feature of the ETS that induces scarcity over time.

Prices subsequently weakened in 2024 as some of those price tensions resolved themselves, higher auction volumes increased the supply of allowances, and power sector decarbonisation continued. By 2025, volatility had largely diminished – as much as 25% less than previous years, according to an analysis by think tank European Roundtable on Climate Change and Sustainable Transition (ERCST) – due to limited policy announcements and weakening of the carbon – gas coupling.

Nevertheless, earlier this year, as speculative purchases of allowances temporarily inflated prices before some European political leaders called the ETS into question, volatility once more returned. In the longer-term, however, the EU appears set to prioritise stability through changes to the Market Stability Reserve (MSR), a mechanism that adjusts the supply of EU ETS allowances.

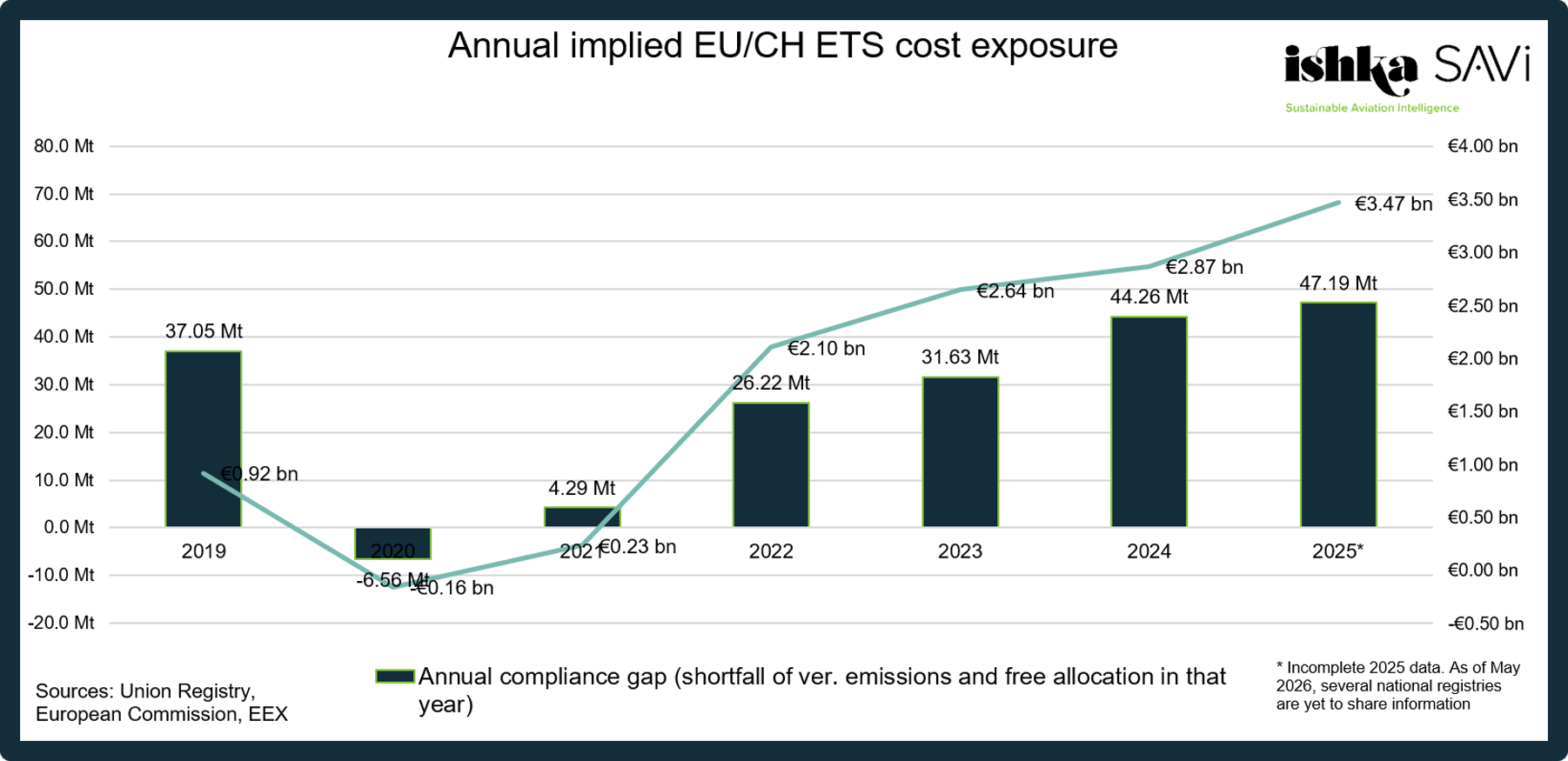

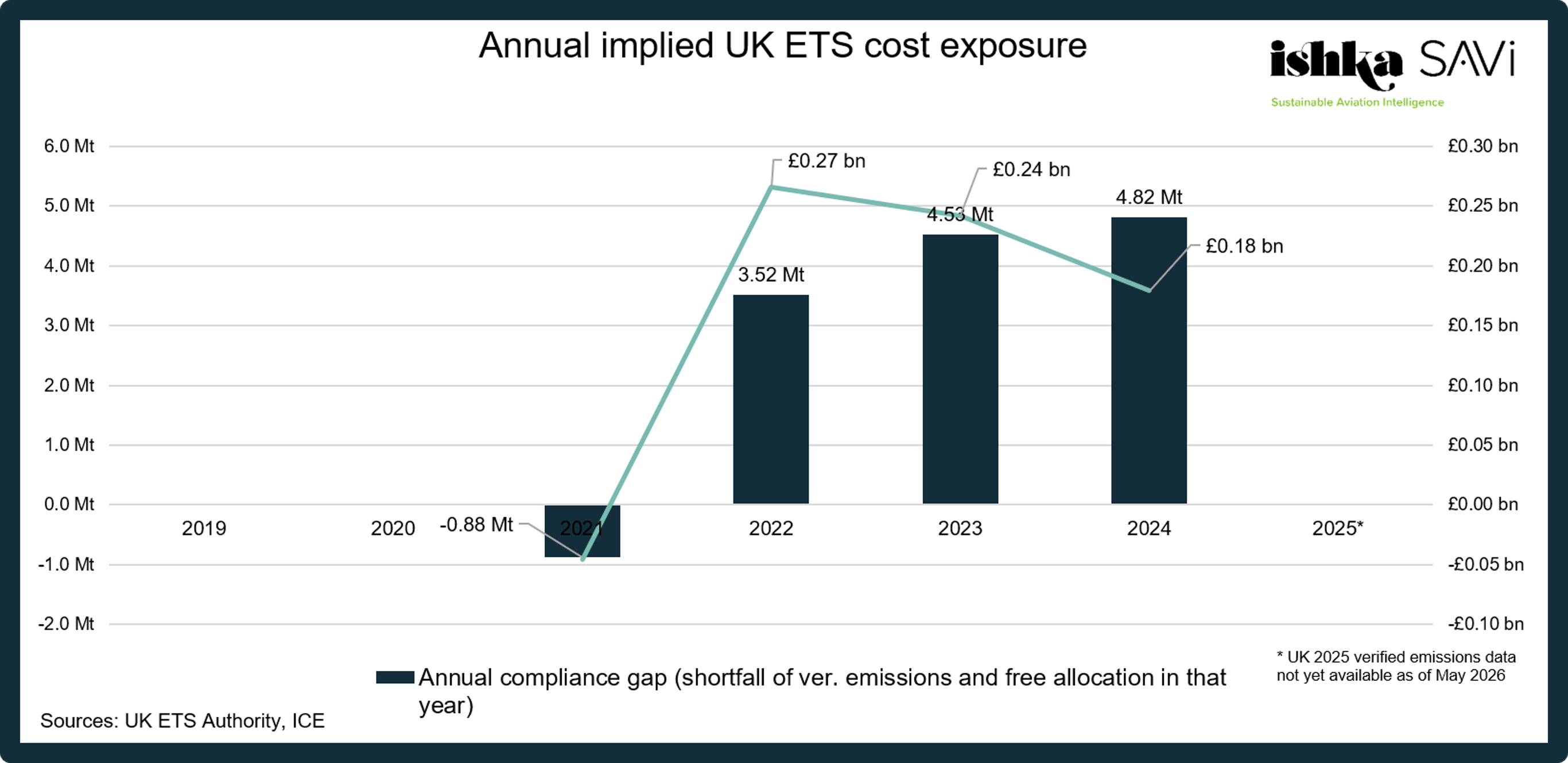

Implied costs for the sector

Note: Calendar-year average prices are used in these charts. Differences between simple calendar-year averages and allowance-weighted averages are negligible for both the EU ETS and UK ETS. Annual implied costs are calculated by applying the average ETS allowance price (EUAs and UKAs) to the annual shortfall between verified emissions and free allocation. As noted previously, 2025 EU ETS verified emissions remain incomplete, as emissions reported to the French ETS authority have not yet been fully incorporated. As a result, the 2025 total is likely understated and will increase once full data are available.

Note: Calendar-year average prices are used in these charts. Differences between simple calendar-year averages and allowance-weighted averages are negligible for both the EU ETS and UK ETS. Annual implied costs are calculated by applying the average ETS allowance price (EUAs and UKAs) to the annual shortfall between verified emissions and free allocation. As noted previously, 2025 EU ETS verified emissions remain incomplete, as emissions reported to the French ETS authority have not yet been fully incorporated. As a result, the 2025 total is likely understated and will increase once full data are available.

The charts above show the approximate compliance cost exposure for airlines operating under the EU and UK ETS since 2019. These figures are illustrative, as airlines can hedge exposure (Ryanair is a good example), opportunistically trade allowances across market cycles, and bank allowances from earlier periods, meaning realised costs may differ materially from annual averages. Coverage is also not perfectly complete: a limited number of flight categories and very small operators are exempt from ETS obligations, although these exemptions are small relative to total aviation emissions covered.

A 2026 cost estimate

Predicting the total costs of EU/CH ETS and UK ETS for airlines in 2026 has become more challenging following developments in the Middle East since 28th February. Higher jet fuel prices, their impact on air traffic demand, and potential adjustments to airline schedules – including reduced deployment of older, less fuel-efficient aircraft – could all influence total emissions in 2026.

For this hypothetical exercise, Ishka SAVi has adopted a simplified approach, assuming 60 Mt based on a rounded-up estimate of provisional EU ETS 2025 verified emissions and 5 Mt based on 2024 UK ETS verified emissions – both the latest available.

Using current carbon prices as a reference (€74.72/EUA and £49.05/UKA), the EU ETS compliance bill could reach approximately €4.48 billion ($5.2 billion) in 2026, while the UK ETS bill could amount to around £245.2 million ($329 million).

The combined $5.5 billion bill is roughly six times airlines’ implied ETS costs in 2026, highlighting the scale of the sector’s growing exposure to carbon pricing and the financial impact of full auctioning requirements.

An upcoming report will explore the impact on individual airlines in more detail.

The Ishka View

The days when the ETS was viewed as a marginal compliance cost for airlines are behind us. Emissions compliance has become a multi-billion-euro expense for Europe's aviation sector, and one that continues to grow. It is therefore unsurprising that several European airlines have intensified their criticism of the system in recent months, calling either for closer alignment with the cost of compliance under CORSIA – a scheme that covers only a portion of international aviation emissions through offsets that currently trade at roughly a third to a fifth of EU ETS allowance prices – or for the reintroduction of free allowances to mitigate competitive distortions.

For now, however, the EU shows little sign of accommodating those demands. Indeed, policymakers may be preparing to propose an expansion of the ETS to cover all flights departing from Europe, a move that could significantly increase compliance costs for long-haul operators and bring non-European airlines within its scope. Prices, too, are expected to continue increasing, even if below initial expectations. BloombergNEF analysts project average EUA prices of €86/t ($87/t) in 2026, rising to €142/t ($165/t) in 2030 and €185/t ($215/t) in 2035.

For airlines, however, rising allowance prices do not necessarily translate into a proportional increase in compliance costs. Since 2024, carriers have been able to claim free ETS allowances to offset part – and in some cases all – of the price premium associated with SAF. The mechanism effectively links decarbonisation efforts with ETS cost relief, reducing airlines' net exposure to higher carbon prices. The European Commission is currently assessing whether to extend the scheme, which, despite some administrative difficulties in its initial implementation, has generally received strong support from the airline industry.